If you are thinking of buying property in Valencia to rent out, one number matters more than any other: the return. How much income will the property really earn against what you paid for it? Every investor asks it, and too often the answer is vague optimism rather than facts.

Let us be brutally honest about rental returns in Valencia. This guide covers how yield works in practice and the crucial gap between gross and net. It maps what yields reach across the city’s neighbourhoods in 2026. And it shows the costs that quietly erode them, plus how to read performance over the long term.

At Homevested we help investors buy in Valencia regularly, and experience tells us one thing: the investors who earn strong rental returns enter with realistic expectations and a firm grip on the numbers. This article helps you build exactly that.

First of All, What Is Rental Yield?

Put simply, rental yield is the annual rent a property earns, shown as a percentage of its value. It is the standard measure of how hard your money works in a buy-to-let, and it lets you compare one property, area or city against another.

The catch is that there are two versions of this figure. Mixing them up is the most common mistake in property investing.

Gross Yield

First, gross yield is the simple headline figure: annual rent divided by property price, times 100. For instance, buy a flat for €200,000 and rent it at €1,000 a month, and you earn €12,000 a year — a gross yield of 6%. It is quick to calculate and easy to compare, but it is not what you actually keep, because it ignores every cost of owning and renting.

Net Yield

By contrast, net yield is the figure that really counts. It takes the annual rent, subtracts the costs of ownership, and shows the result as a percentage of your total investment, including purchase taxes and fees. Net yield is always lower than gross — often by 1 to 2 points in Valencia. Any investor or agent quoting only a gross number is flattering the deal, knowingly or not. Always work out the net.

What Rental Returns Look Like in Valencia in 2026

Here is the good news: Valencia is one of Spain’s leading cities for rental returns.

As 2026 begins, Valencia’s average gross rental yield sits around 5.8% to 6.4%, depending on the source. That compares well with Madrid (roughly 4.5% to 5%) and Barcelona (around 4.8%). The reason is simple: price per square metre in Valencia is still lower than in Spain’s two biggest cities, while rents have risen sharply. You can sense-check current data on Idealista’s price reports.

But that average hides a wide range. Yields in prime central Valencia run around 3.8% to 4.5%, held down by high purchase prices, while districts with more renters can reach 7% or more. There is at least a two-point gap between the highest and lowest neighbourhood yields. So “a Valencia yield” means little — what matters is the yield of a specific property in a specific area.

Realistically, most Valencia investors land on a net yield of about 3.5% to 4.5% after costs. Those are solid, safe rental returns, and with the capital growth Valencia has delivered, attractive ones. It is nowhere near the inflated 8% to 10% figures sometimes thrown around. Good investing starts with realistic expectations.

Why Yields Vary So Much Between Neighbourhoods

Knowing how and where rental returns vary helps you choose with intent, rather than chase the biggest headline number.

Prime central districts — the most prestigious, most desirable addresses — tend to return the lowest yields. It sounds paradoxical, but the logic is simple: you pay for prestige, lifestyle and scarcity, and that premium inflates the price faster than the rent. You buy these areas for capital growth and security, not yield.

Mid-priced and working-class areas, plus student districts, deliver the strongest yields. Purchase prices stay affordable while rental demand runs high and reliable, from local tenants and students alike. The rent-to-price ratio is simply better.

Emerging and peripheral districts offer an attractive middle ground. As the city pushes outward, several are seeing fast capital growth that can pair good yield with high upside, though with a little more risk.

The same pattern holds by property type: the smaller the unit, the higher the yield. A studio or one-bed costs less to buy and earns more per square metre, so the ratio favours the investor. Larger two- and three-bed flats are less profitable but more likely to attract long-term family tenants.

The lesson: high income and high appreciation rarely sit on the same property. Decide whether you want income now or capital gains later, and let that guide what you buy.

The Costs That Eat Into Your Rental Returns

This is the section that turns gross into net, and where investors most often fall short. To work out your real rental returns, factor in the costs below.

Acquisition costs. Before the property earns a cent, buying it costs money. In the Valencian Community, transfer tax (ITP) on resale property runs to a meaningful percentage of the price, or VAT at 10% on new builds. On top come notary, registry, legal and gestoría fees. These swell the denominator of your yield, which is exactly why net yield is based on total capital employed, not just the price.

Property tax (IBI). The annual local property tax.

Community fees. Monthly payments for the shared building, varying with the facilities.

Management fees. If you use a manager — which you should if you are non-resident — budget around 8% to 12% of the rent for long-term lets, plus IVA.

Maintenance and repairs. A sensible rule is to set aside part of the annual rent each year, whether or not anything breaks.

Insurance. Buildings cover and, ideally, landlord insurance.

Income tax. Rental income is taxed — residents under IRPF, non-residents under IRNR — with different rates and deductions, so plan it with a tax adviser.

Vacancy. No property is let 100% of the time. Between tenancies you earn nothing while still paying community fees, IBI and any mortgage. Realistic forecasts allow for it.

Add it all up and you can see why costs typically trim 1 to 2 or more points off the gross yield. A 6% gross turning into a 4% net is not pessimism — it is arithmetic.

Long-Term vs Short-Term Rentals

Another common question: does short-term holiday letting beat a long-term tenancy?

At first glance, short-term rentals earn more gross income per month, especially in central, tourist-friendly areas. But the headline hides the reality. Short lets carry higher running costs: cleaning, linen, utilities, furniture and more maintenance. Management fees climb to 20% to 35%, the income swings with the season, and — most important — the rules keep tightening. Tourist licences in Spanish cities are evolving and are not always even available.

A long-term rental earns less gross but offers far more: a steady monthly figure, lower costs, less management, and a simpler legal position. For most investors, especially those who want truly passive, predictable rental returns, a well-placed long-term rental is the more reliable base. Short lets can beat it, but they are more intensive, more uncertain, and more heavily regulated.

A Worked Example: From Headline Rent to Money in Your Pocket

Numbers in the abstract are easy to nod at and hard to absorb. So here is a simplified example — no guaranteed results, just the shape of how money moves from gross to net.

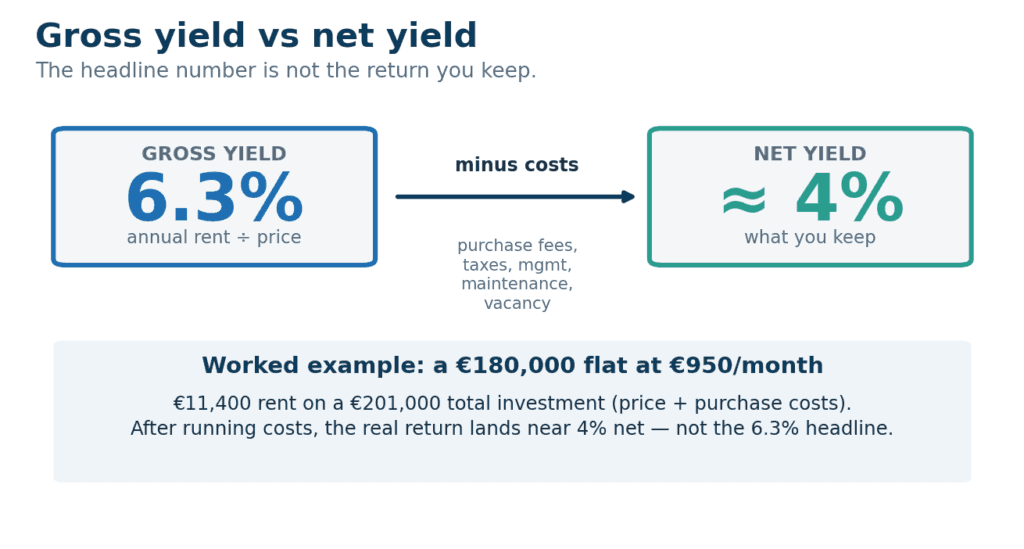

For example, an investor buys a one-bed in a solid mid-value Valencia neighbourhood for €180,000 and secures a reliable long-term tenant at €950 a month, or €11,400 a year. On a gross basis that looks like €11,400 ÷ €180,000 = 6.3% — an attractive headline.

Then reality arrives. The purchase cost more than €180,000: transfer tax, notary, registry, legal and gestoría fees can realistically add around 11% to 13%, roughly €21,000, for a total investment near €201,000. Then come the annual running costs. They include IBI, community fees, management at about 10% plus VAT, a maintenance and insurance reserve, void periods, and income tax on the profit. Once you account for everything, the real rental returns on that €201,000 land near 4% net, not the 6.3% gross headline.

Of course, the point is not that the deal is poor. A 4% net yield on a stable, appreciating asset in a buoyant market is genuinely attractive. The point is that 6.3% was never the true figure, and any investor who budgeted their life around it would end up disappointed. Always work out the net before you buy.

Common Mistakes Investors Make

In practice, a handful of errors come up again and again. Planning around them is some of the cheapest insurance there is.

- Trusting the gross yield. A slick “6% yield!” is a gross figure. Knock off a point or two before you even consider it.

- Ignoring purchase costs. Taxes and fees on the way in are real, permanent money and belong in your return calculation. Measuring yield against price alone flatters the deal.

- Assuming 100% occupancy. No property is let forever. Tenancies start and end, and finding the right new tenant takes time. Build in a vacancy rate.

- Underbudgeting maintenance. A prudent reserve is what stops one bad year from wrecking the average.

- Chasing yield into the wrong property. The top gross yields often come with higher tenant turnover, weaker capital growth or heavier management. The biggest number on a spreadsheet is not always the best investment.

- Overlooking tax. How rental income is taxed and what is deductible depends on residence and structure. Planning ahead keeps more of your return.

- Ignoring local knowledge. Buying in a foreign city on internet averages alone is how avoidable mistakes happen. There is no substitute for local insight on pricing, demand and neighbourhoods.

Avoiding these takes no genius — just discipline, grounded numbers and good advice.

Who Rents in Valencia?

Rental returns are only as strong as the demand behind them. No property earns a cent without a real person who wants to live in it, so it pays to know who actually rents in Valencia. A broad, stable tenant base means fewer voids and steadier rent.

In general, Valencia has an unusually broad, stable rental market. First, local residents who see the city as home form a steady core. Students are the next big group: as a university city, student-heavy districts see reliable, recurring demand year after year, which often lifts yields. Internal relocations add more.

Then there is the wave of international residents that has reshaped the city. Valencia is now a top European draw for foreigners, remote workers and digital nomads, pulled in by the weather, lifestyle, affordability and manageable size. Many rent first — sometimes for a year or more — before deciding whether and where to buy. They form a constant, valuable pool, especially for quality city-centre apartments.

The practical upshot is resilience. Even if one group pulls back, Valencia has plenty of other renters, so the income stream is less exposed to a single shift and far more sustainable. It also raises a real choice: a flat aimed at long-term local professionals performs very differently from one aimed at students or short-stay arrivals. Matching the property to the tenant pool you want is sensible management, not wishful thinking.

Beyond Yield: The Total Return Picture

Your rental returns are about more than yield. Total return combines two things: rental income, the yield we have discussed, and capital appreciation, the rise in the property’s value over time.

Indeed, Valencia has seen healthy price growth in recent years, with strong gains expected through the end of 2025 and more modest growth into 2026. For an investor earning a 4% net yield on top of steady appreciation, the total return sits well above the yield figure alone.

Moreover, property has another quieter advantage: over the long run it is widely seen as a good inflation hedge. Values and rents have historically risen broadly in line with, or ahead of, inflation. That helps protect the real value of your capital in a way cash in the bank cannot. Property is not a quick flip; its benefits show over years, through income, appreciation and inflation protection.

None of this is guaranteed — markets move, and past patterns never promise future results. But it is why so many investors treat a Valencia property as a long-term hold rather than a quick profit.

How to Improve Your Rental Returns in Valencia

Your rental returns are not fixed at purchase. Several decisions can meaningfully improve them:

- Buy well. The biggest lever of all. The price you pay forms the denominator of every yield calculation, forever. A disciplined, well-researched purchase at a fair price beats years of fiddling later.

- Choose the area carefully. Pick a property that fits your goal — higher income, higher growth, or a balance of both.

- Minimise vacancies. Every empty week is lost return. Keep the property well maintained, fairly priced and actively managed.

- Screen tenants thoroughly. A reliable, long-term tenant who pays on time and respects the property protects your return more than chasing the highest rent.

- Control your costs. Sensible community fees, efficient upkeep and good management all feed straight into your bottom line.

- Add value where it pays. A smart refurbishment and a better energy rating can lift both the achievable rent and the resale value.

- Get the tax structure right. How you hold the property and report income affects your net return. Professional advice often pays for itself.

A Word on Financing and Leverage

So far we have mostly assumed a cash purchase. Many investors use a mortgage, and its effect on returns is worth understanding.

The idea is leverage. Borrowing to part-fund the purchase means less of your own money goes in, which can lift the return on the cash you do invest. If the net yield comfortably beats the mortgage cost, the difference works in your favour, and your return on equity can exceed the property’s own net yield. That is one of property’s classic attractions.

But leverage cuts both ways. A mortgage is a fixed monthly obligation, due whether the property is full or empty. Borrowing costs reduce your net income, and if values fall, leverage magnifies the loss just as it magnifies the gain. Financing also adds cost and complication, and the terms offered to non-residents differ from those offered to residents. The smart approach is neither to avoid debt entirely nor to over-borrow to outdo your neighbour. Instead, treat leverage as a precision tool: handled professionally, used cautiously, and sized to an investment that stays comfortable even in a poor year. Discuss it with an experienced mortgage and tax professional before you commit.

Thinking Ahead: Your Exit and the Long View

Total return is not just about how the property performs while you own it — it is about how the investment ends.

Ultimately, property is inherently long-term. Transaction costs on each side of a deal reward patience and punish quick flips. The investors who succeed in a market like Valencia tend to share a pattern. They buy a good property at a fair price and hold it for a decade or more. They gather rental and capital gains over time, and sell when it suits their wider plan rather than too early.

It helps to know from the start that selling has costs too: capital gains tax on a profit, the local Plusvalía tax, and others. So judge a property over its whole life, from purchase to eventual sale, rather than over a single year’s rent.

That long view reframes the yield itself. A 4% net may sound modest on its own. But picture 4% income, every year, from a property that is also appreciating and acts as an inflation hedge. Held patiently for ten years or more, that is the foundation of real, durable wealth. The headline percentage only ever tells part of the story. The other part is time.

How Homevested Helps Investors in Valencia

Homevested looks at the Valencia market through this lens and helps investors enter it with eyes open and numbers realistic. We handle the investment search and buying side, finding the right kind of property for your goal and being honest about the rental returns you can expect.

A return only materialises if the property is managed well. So our property management team takes over the day-to-day — tenant sourcing and retention, rent collection, maintenance and compliance — to protect your net yield over the long term. We are a popular choice for offshore and overseas investors who want a genuinely passive investment in one of the world’s most dynamic property markets. To go deeper, see our guides to property management in Valencia and valuing a Valencia property.

Frequently Asked Questions

What are good rental returns in Valencia?

In 2026, gross rental returns in Valencia average roughly 5.8% to 6.4%, on the higher side compared with Madrid and Barcelona. After costs, net returns realistically run around 3.5% to 4.5%. What counts as “good” depends on your goal: prime central areas offer lower yields but stronger appreciation, while lower-priced, renter-heavy areas offer higher yields.

What is the difference between gross and net yield?

Gross yield is annual rent as a percentage of the property price — a simple headline that ignores costs. Net yield subtracts all ownership costs (taxes, fees, management, maintenance, vacancy) and shows the result against your total investment, including purchase costs. Net yield is what you actually earn, and in Valencia it usually runs 1 to 2 points below gross.

Where in Valencia gives the highest yields?

The highest gross yields tend to come from lower-priced districts with more renters and students, where entry prices are lower and demand is high. Yields there can top 7%. The priciest central areas have the lowest yields, often below 4.5%, though they usually outperform on capital growth.

Is short-term or long-term letting more profitable in Valencia?

Short-term holiday lets can earn much more gross income, but with far higher costs and fees, a more volatile income stream, and a tighter, more restrictive licensing regime. Long-term rentals earn less gross but are more stable, cheaper to run and simpler legally. For a passive investor, a well-placed long-term rental is usually the more dependable income.

What should I subtract from my rental yield?

In order of weight: purchase taxes and fees, annual property tax (IBI), community fees, management fees, maintenance, insurance, income tax, and vacancy between tenancies. Together these typically take 1 to 2+ points off the gross yield, which is why the net is so much lower.

Is Valencia property a sound long-term investment?

Valencia has offered strong rental yields and excellent capital growth, and property has long served as an effective inflation hedge. Total return, income plus growth, has been attractive. But returns are not guaranteed, markets move, and success ultimately rests on buying well and managing wisely. Realistic projections and good professional advice are essential.

Talk to Homevested About Investing in Valencia

Solid property investment starts with solid numbers and ends with solid management. Homevested can help with both — identifying the right investment for your strategy, then managing it so your projected return becomes your actual return. If you are weighing a buy-to-let in Valencia, get in touch and we will run the real figures with you, not just the flattering ones.